- June 19, 2026

-

-

Loading

Loading

One of the hallmarks of Longboat Key town government over the past 25 years has been the town’s fiscal strength and conservatism.

Town commissioners and the town administration have managed Longboat taxpayers’ money well. So well, in fact, the town’s “unrestricted general fund balance” (its rainy-day savings funds) totaled 54%, or roughly $8.5 million, of a $16 million general fund budget for the year ending Sept. 30, 2018. That’s 3.3 times more than town ordinances require.

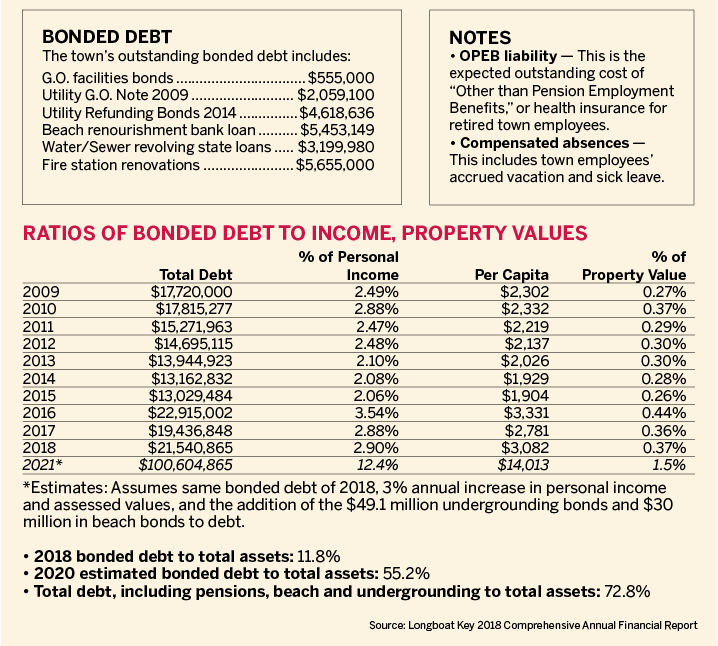

And if you track the town’s long-term debt over the past decade (see bottom table below), from 2009 through 2015, the town consistently held its borrowing in check.

You can even credit former Town Manager David Bullock for ending the town’s disastrous defined-benefit pension plan for new town employees in 2012 and 2013. That kept the town from digging an even deeper debt hole, though the town’s unfunded pension liabilities still stand at around $28 million as of Sept. 30, 2018.

Had Bullock not done that, the town could be in the same position today as the city of Sarasota, where its unfunded pension liabilities exceed $100 million.

However, the town’s overall finances are in good shape. Standard & Poor’s gave the town’s general obligation bonds an AA+ rating. But the fact the town’s total assessed value stands at $6.15 billion and its millage rates are only 2.8 mills for gulfside owners and 2.3 mills for bayside owners, the town has plenty of room to raise taxes if it needs more money.

Nevertheless, it’s worth noting a sudden ballooning of town debt — all of which taxpayers must service through property taxes and assessments.

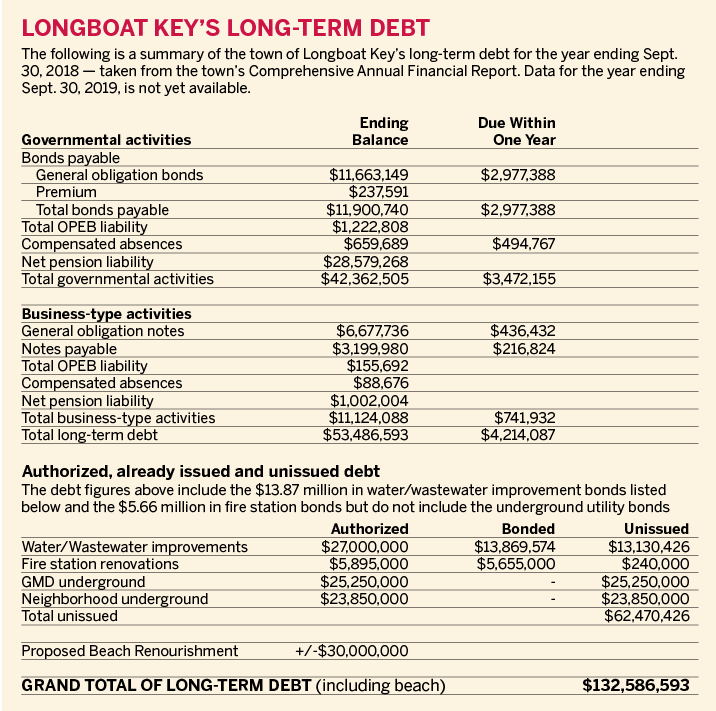

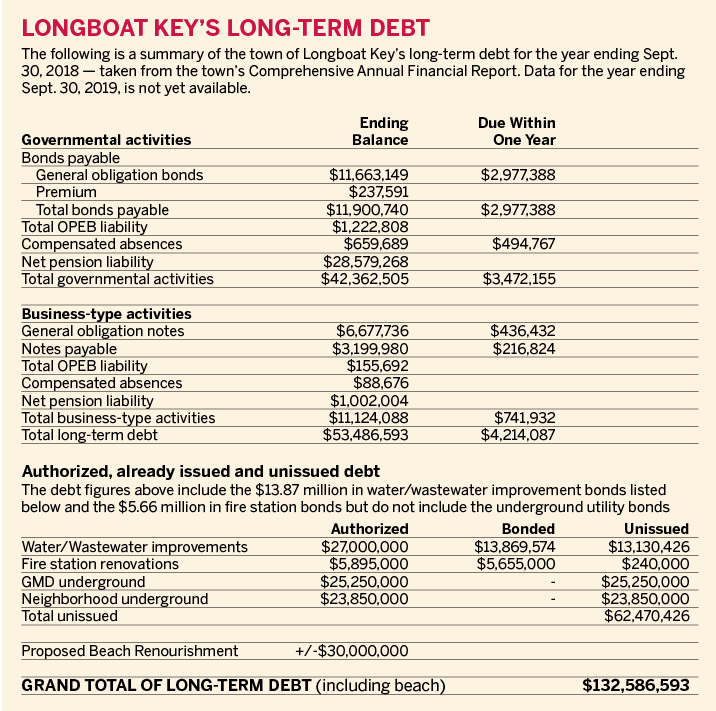

Let’s start at the top of the accompanying box. As of the year ending Sept. 30, 2018, the most recent published data available. The town’s total long-term debt — bonded debt and unfunded pension liabilities — totaled $53.48 million.

That figure did not include the $49.1 million in bonded debt that will fund the installation of the town’s underground utilities over the next two years.

Nor does it include the $25 million to $32 million for the next beach renourishment. Voters will decide next March exactly how much the town will bond for the 2021 beach renourishment project. It looks like the amount will fall between $25 million and $32 million.

Now take a breath and compute all of these numbers. When you add everything together — current outstanding bonded debt, unfunded pension liabilities, the two underground utility projects and the 2021 beach renourishment — the town’s true long-term debt is about to mushroom to more than $132 million. Bonded debt will exceed $100 million.

For a town of 7,000 population and an annual general fund budget of $16 million, that’s a staggering jump in borrowing.

Will it mean the town’s finances suddenly will go from good to shaky?

No. But it does mean Longboat’s property owners are going to be paying more in property taxes and assessments to cover roughly $80 million in new debt (underground plus beach).

This should and likely will spark some careful and cautious considerations on the part of the Town Commission.

In every business, there is a threshold as to how much the staff can handle well at once. In the case of Longboat Key over the next two to three years, the town staff’s project list and the town’s financial obligations will be greater than they have been in a quarter century — underground utilities, major beach renourishment, renovated fire stations, reconstruction of the infrastructure in Emerald Harbor and what to do about pickleball courts.

The proposed town center is also on that list. And there are commissioners who remain optimistic the town will find private-sector funding to build it.

If that doesn’t materialize, we hope commissioners take into account there is only so much debt taxpayers are willing to carry.