- June 19, 2026

-

-

Loading

Loading

Gov. Ron DeSantis is set to sign the annual state budget bill any day. One bright spot within the bill is the fixes it presents for the state worker retirement system. The Florida Retirement System (FRS) has been in trouble for years. Inadequate contributions built up $30 billion in debt, putting workers’ retirement security and taxpayers’ wallets at risk. While legislative reforms in recent years helped stop the bleeding, they created new challenges. Now, those challenges are being tackled.

The budget approved by the Florida Legislature would improve the defined contribution retirement benefit provided to all recent state workers. When created, the default defined contribution retirement plan provided the worst benefit among all such state-run retirement plans in the nation. The changes found in the budget help by giving a 3% benefit increase to all active plan members, creating a more sustainable retirement benefit while reducing a big risk to taxpayers. Over 180,000 educators, administrators, and other government workers are slated to receive the additional 3%, effective July of 2022.

In combination with previous reforms, the new rules in the budget make Florida a leader in providing attractive, choice-based, affordable benefits to an increasingly flexible and diverse workforce. The change also improves the footing of the state’s defined contribution plan, which plays a critical role in addressing the financial risks borne by public employers and taxpayers. These changes address a long-standing problem.

Originally adopted during the 2000 legislative session as an alternative option to the state’s traditional defined benefit pension, the state defined contribution plan — Florida Retirement System Investment Plan (FRS IP )— has taken on increasing importance in Florida state and local government administration and now serves as the state’s primary vehicle for providing retirement security to most public workers.

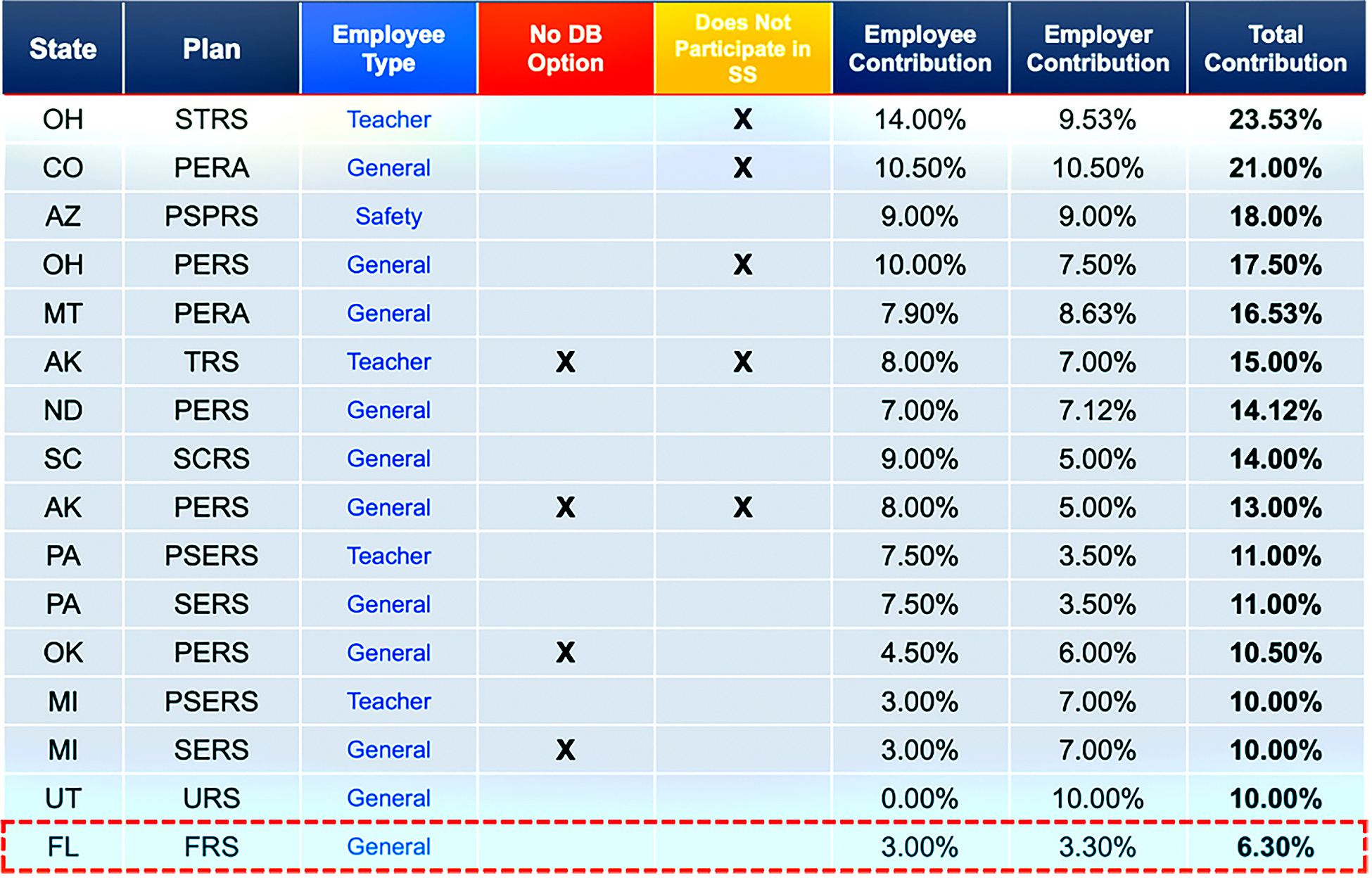

With so many teachers and public employees dependent on the FRS IP as a means to support retirement, it is crucial that the default retirement plan provide sufficient contributions to allow workers to make continuous progress toward saving for a healthy and comfortable post-employment lifestyle. Financial advisors and industry experts typically recommend total contributions into a plan like the FRS IP should total at least 10% of an employee’s pay (many even prefer 12% to 15% to ensure benefit adequacy) for the eventual benefits to be sufficient for retirement.

For over two decades, Florida’s public employers at the state and local levels were required to contribute 3.3% of an employee’s salary to their FRS IP account for the largest grouping of employees (Regular Class), which includes teachers and most civilian government employees. Employees in turn contributed a fixed 3% of their pay to their FRS IP account to bring the historic savings rate of FRS IP members to 6.3%, far below industry standards. This combination places Florida well below other states who offer defined contribution plans, further highlighting the need to address the funding flowing into the IP.

Insufficient contributions to a public retirement plan should be a major concern for employees, policymakers, and taxpayers alike. A generation of retirees inadequately prepared for retirement creates a risk of increased reliance on the state’s social safety net. This shortcoming also creates more immediate challenges that can impact many stakeholders. Benefits below industry standards and below those available in the private sector can significantly hinder the state’s ability to compete for talent, especially in areas like information technology and data security, to ensure the continued delivery of quality public services to Floridians

For FRS Investment Plan members, the reforms in the budget increases the employer contribution to employee IP accounts by 3% of payroll over current levels and covers all membership classes. All present and future members of the FRS IP will see an equal increase. The largest grouping of employees —Regular Class (which includes teachers and most non-public safety workers) — will see the employer rates into their IP accounts rise from 3.3% of pay to 6.3%. In combination with their own 3% contribution, which will remain unchanged, the total into the IP plan for Regular Class members will now be 9.3%. Those in the Special Risk Class, which includes public safety officers, will see their total contributions rise from 14% to 17%.

According to the House’s fiscal analysis of the budget, the 3% increase of employer contributions into the FRS IP is estimated to require an additional $249 million in the first year from all state and local government employers. These changes would move the state into a more competitive position by providing employees more resources to meet their retirement needs. The increased amount employers will contribute to their employees’ FRS IP accounts comes on the heels of lawmakers also agreeing to 5.38% across the board pay increases for public employees. For those participating in the FRS Investment Plan, this will bring the total increase in compensation to more than 8%.

States around the country are scrambling to recruit employees. These changes will make Florida a more competitive option for new workers, especially highly skilled technical professionals the state expects it will need in the future.

Florida policymakers and those involved in this reform process deserve credit. But this should not be the end of thoughtful improvements to the state’s retirement system. To build on this session’s success and remain competitive with the private sector, stakeholders should continue searching for ways the FRS IP can better serve public employees. There are several clear opportunities:

First, is setting some clear objectives. The Florida Retirement System as a whole is governed by a set of objectives, but the nature of its two retirement options presents an opportunity for additional mission clarity and transparency. Specific language delineating new objectives, such as lifetime income and retirement security, could help communicate the goals of the plan to new and existing public workers.

Second, improve the investment mix. Well-designed plans like the FRS IP should also offer the correct age-appropriate investment mix. This is generally accomplished by using target date funds that adjust investment risk to the employee’s retirement horizon. Given the serious role these funds play in the lives of public workers and their families, protecting the value of a member’s FRS IP account from market fluctuations as the worker nears retirement should be a high priority.

Providing annuities to improve members’ retirement security has long been an established practice in the FRS IP but could still be improved. Offering annuitization at retirement allows retirees to use their accrued retirement funds to buy a stream of guaranteed income. Despite a lifetime annuity option being available to members already, distribution choices offered by the FRS IP are limited. Expanding those offerings to include deferred annuities could present an opportunity to further improve this offering.

Third, budget reform would bring total contributions nearly, but not quite, to the 10% minimum standard set by industry experts. Despite the prudent dedication of funds to address this pressing issue, Florida will still be below all other states in total contributions for most members of the FRS IP. There is still room for improvement in this regard, and it may be prudent to consider ways to increase the fixed employee contribution toward their own retirement. Lawmakers should recognize that with future efforts, they can build upon the benefits that will come from this latest legislation.

We should all appreciate the pension system reforms in the proposed state budget and encourage the governor and state legislature to keep up the good work.

Adrian Moore, Ph.D., is vice president of Reason Foundation and lives in Sarasota.